Bank Statement vs Bank Reconciliation: Key Differences

Accounting terms and jargon might seem confusing if you’re not used to dealing with banking. This includes things like bank statements, bank reconciliations, and equity statements, among others.

In this blog, we’re going to simplify these terms for you. We’ll explain what they’re for, how they differ from each other, and why they’re important in banking.

Key Takeaways:

- Bank Statement: A record from the bank listing all transactions in an account over a specific period, such as deposits, withdrawals, fees, and interest, serving as an official account activity snapshot.

- Bank Reconciliation: A process by the account holder comparing their financial records against the bank’s statement to ensure accuracy and identify any discrepancies or unrecorded transactions.

- Key Differences: Bank statements are issued by the bank and list transactions, while bank reconciliations are conducted by the account holder to match records and identify discrepancies.

- Importance: Both are crucial for financial management; bank statements help track transactions and manage finances, while reconciliations ensure record accuracy and highlight potential fraud.

- Process: Reconciliation involves matching transactions between bank statements and personal records, identifying discrepancies, and adjusting balances to ensure accurate financial records.

While you are here

Reconcile bank statements automatically

DocuClipper extracts every transaction and validates totals against opening and closing balances. Catch gaps before they become audit findings.

What is a Bank Statement?

A bank statement is a paper or digital record from your bank that lists all the money going in and out of your account for a certain time, usually a month. This record shows deposits, withdrawals, any charges the bank has made, and any interest you’ve earned.

You can use statements during bank statement analysis to keep an eye on your money, make sure all the bank transactions are right, and spot any strange or wrong transactions.

What is a Bank Reconciliation?

Bank reconciliation is when you or your finance team check your financial records against the bank’s statement. It is to process bank statements and check each detail present to it.

This is to make sure all transactions match up and to find any mistakes or transactions that were missed, either in your records or the bank’s.

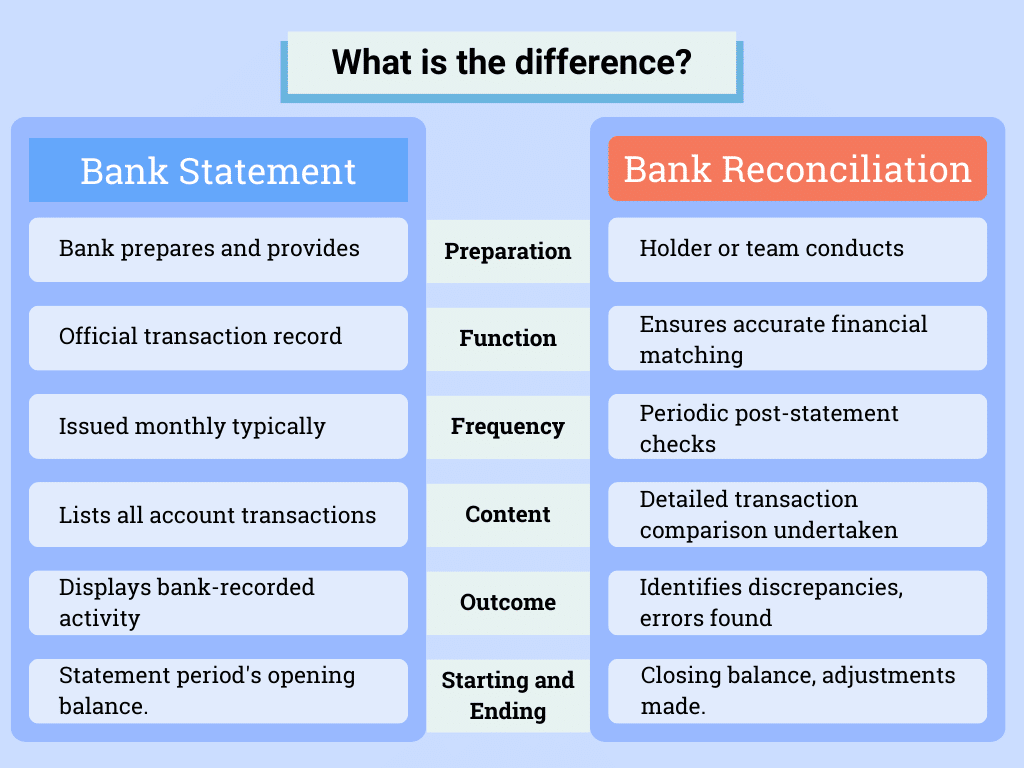

Key Differences Between Bank Statement and Bank Reconciliation

Both of these terms are frequently used in accounting and finance, but if you’re not aware of what they mean and what makes them different, then you will struggle to complete basic accounting tasks.

Therefore, here are some notable differences between bank statements and bank statement reconciliations:

| Aspects | Bank Statement | Bank Reconciliation |

| Nature | A document issued by the bank, detailing account transactions over a specific period. | A process is undertaken by the account holder to compare their records with the bank statement. |

| Preparation | Prepared and provided by the bank. | Conducted by the account holder or their financial team. |

| Function | Serves as an official bank record of all transactions in an account. | Aims to ensure the account holder’s financial records match those of the bank. |

| Frequency | Typically issued monthly. | Performed periodically, often monthly, after receiving the bank statement. |

| Content | Lists transactions such as deposits, withdrawals, fees, and interest. | Involves the detailed comparison of transactions on the bank statement with the account holder’s records. |

| Outcome | Shows the account activity as recorded by the bank. | Identifies discrepancies, unrecorded transactions, and potential errors in record-keeping. |

| Starting Amount | The opening balance at the beginning of the statement periods | The account balance is according to the account holder’s records at the beginning of reconciliation. |

| Ending Amount | The closing balance at the end of the statement period. | The adjusted balance after accounting for discrepancies and unrecorded transactions. |

Nature

Bank Statement: A factual record provided by the bank. It lists all transactions in your account for a specified period, like deposits, withdrawals, and fees. This document serves as an official snapshot of your account’s financial activity.

Bank Reconciliation: An analytical process performed by the account holder or their financial team. This involves comparing your financial records against the bank’s statement to ensure accuracy. It helps identify discrepancies, such as missed transactions or errors in recording.

Preparation

Bank Statement: These are typically provided by the bank automatically. Minimal preparation is required for them as they have everything stored digitally and can be printed or sent in neat formats.

Bank Reconciliation: These are prepared by accounting officers or business owners. It requires many documents not only bank statements but also invoices, and revenue records.

Function

Bank Statement: Serves as an account of transactions processed by the bank. It provides a detailed overview of all financial movements in your account, helping you track your balance and transaction history. It is a tool for reviewing your financial status as recorded by the bank.

Bank Reconciliation: Aimed at verifying the accuracy of your financial records. By comparing these records with the bank statement, it ensures that every transaction is accounted for and correctly recorded. This process helps in maintaining accurate and up-to-date financial records.

Frequency

Bank Statement: Typically issued monthly by banks. It’s a periodic record that arrives regularly, allowing account holders to review their account activity over the last month. Some banks also offer options to access statements more frequently online.

Bank Reconciliation: Carried out regularly by the account holder, often monthly or quarterly. This process is initiated by the account holder following the receipt of a bank statement. The frequency can vary based on personal or business needs for financial oversight.

Content

Bank Statement: Provides a comprehensive list of all transactions, including deposits, withdrawals, fees, and interest, recorded over a specified period. It’s a detailed documentation of your account’s activity, reflecting every financial move as tracked by the bank.

Bank Reconciliation: This involves a detailed comparison of your financial records against the bank’s statements. This process checks each transaction for consistency, aiming to match your accounting records with the bank’s recorded transactions.

Outcome

Bank Statement: The outcome is an official record that gives you a clear view of your financial transactions as per the bank’s records. It serves as a reliable source for understanding your account’s activity and financial status at a glance.

Bank Reconciliation: The primary outcome is the identification and correction of any discrepancies between your records and the bank’s. This ensures the accuracy of your financial records, highlighting errors or unrecorded transactions for resolution.

Starting Amount

Bank Statement: The balance of your account at the beginning of the statement period.

Bank Reconciliation: The recorded balance before the reconciliation process begins.

Final Amount

Bank Statement: The balance at the end of the statement period, after accounting for all transactions.

Bank Reconciliation: The adjusted balance after accounting for discrepancies found during reconciliation.

Summary of Bank Statement vs Bank Reconciliation

Bank statements and bank reconciliations are two important tools that help you keep track of your money. A bank statement is a list from your bank that shows all the money that went in and out of your account during a certain time, usually a month. It helps you see what you have spent and what you have earned.

Bank reconciliation is like doing a bank statement audit. This is done to make sure everything matches up and to find any mistakes or things that were missed, like payments or deposits that didn’t show up on the statement.

The main point of doing a bank reconciliation is to make sure your records are right. If you find any differences between your records and the bank statement, you can fix them. This helps you know exactly how much money you have and keeps your financial information accurate.

Why Both Are Important in Accounting?

Both of these are different and important in their own way. Accountants and business owners consider these as vital information as these can be the basis of their financial advice and their business decisions.

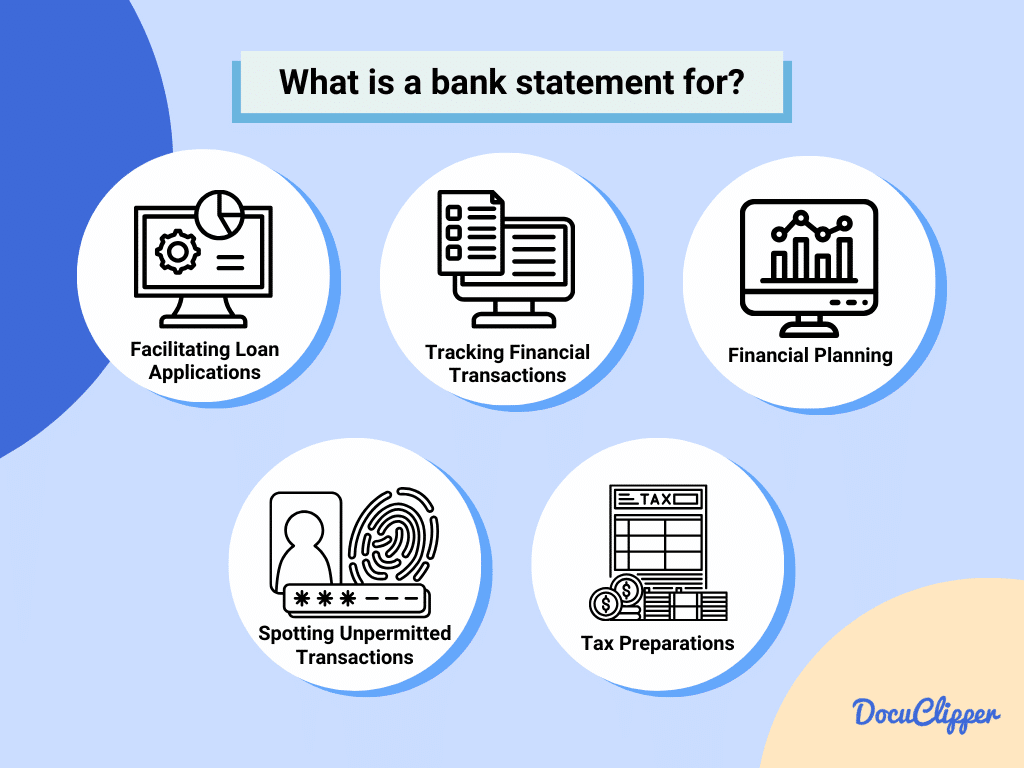

Role of Bank Statements in Financial Management

Here are the main reasons why bank statements are important for businesses and accountants:

- Tracking Financial Transactions: This helps you keep track of your money coming in and going out.

- Budgeting and Financial Planning: Essential for managing your finances effectively.

- Detecting Unauthorized Transactions: Helps spot any fraudulent activity on your account quickly.

- Supporting Tax Preparation and Filing: Provides necessary information for accurate tax returns.

- Facilitating Loan Applications and Credit Requests: Banks often require recent statements when you apply for loans or credit.

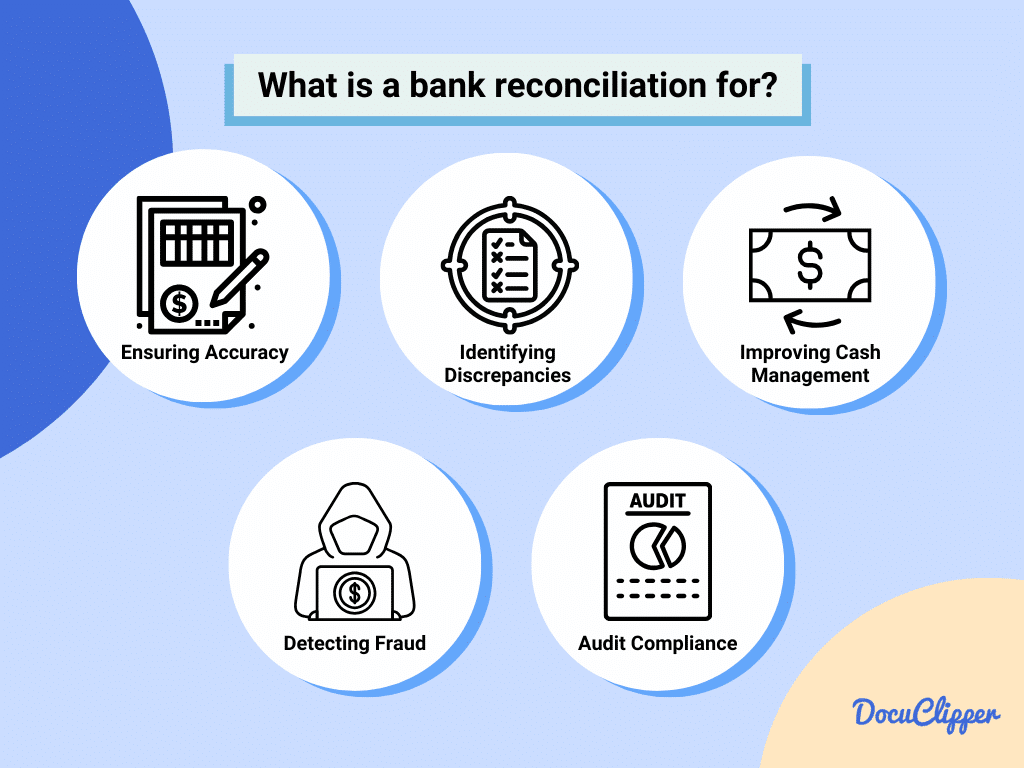

Role of Bank Reconciliation in Financial Management

Here are some main reasons why bank reconciliation is important for businesses and accounting professionals:

- Ensuring Accuracy of Financial Records: Guarantees that your records match the bank’s.

- Identifying Discrepancies and Errors: Helps catch mistakes or omissions in your or the bank’s records.

- Detecting Fraud: This can reveal fraudulent activities if there are transactions you don’t recognize.

- Improving Cash Flow Management: Provides a true picture of your cash status.

- Compliance and Audit Readiness: Ensures your financial records are accurate and audit-ready.

Put it into practice

Reconciliation errors start in extraction

Split rows, missed transactions, and rounded figures compound over time. Structured extraction with built-in validation gives you a reconciled result from the first pass.

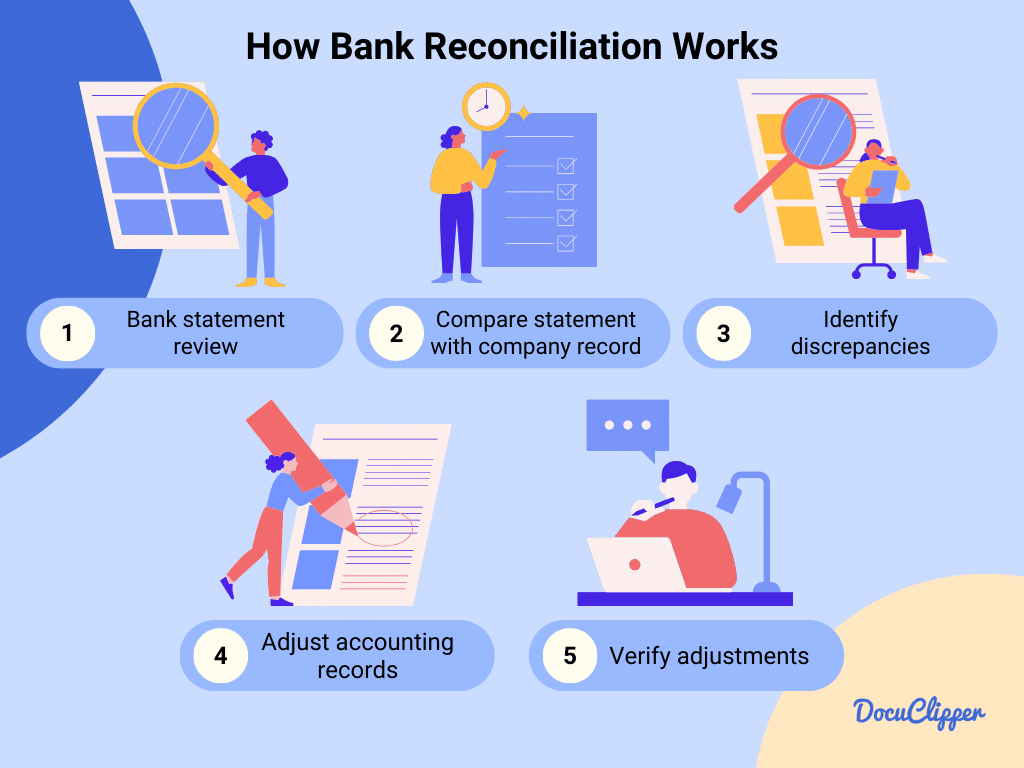

How to Reconcile a Bank Statement?

Reconciling bank statements might seem daunting at first, but it’s a crucial process for maintaining accurate financial records. Here’s how to do it in simple steps:

- Collect Your Records: Gather your bank statement and your financial records, such as your checkbook register or accounting software reports.

- Check the Starting Balances: Make sure the starting balance of your records matches the starting balance on the bank statement.

- Match Transactions: Compare each transaction on your bank statement with your records. Check off each one that matches.

- Identify Discrepancies: Look for any transactions that are in your records but not on the bank statement and vice versa. These could be outstanding checks, deposits in transit, or bank errors.

- Adjust Your Balance: Adjust your records for any transactions that haven’t yet appeared on the bank statement. Add deposits in transit to your balance, and subtract outstanding checks.

- Account for Fees and Interest: Add any interest earned and subtract any fees or charges that appear on the bank statement but not in your records.

- Finalize the Reconciliation: Once every transaction has been accounted for and your adjusted balance matches the bank statement’s closing balance, your bank statement is reconciled.

A faster way to do this is to use a bank statement converter that has features that help in reconciling bank statements. One of these OCR software that specializes in bank statements is DocuClipper

Conclusion

Bank statements and bank reconciliation are both key for keeping track of your money, but they serve different purposes. These should not be easily confused and they are simpler than they sound.

A bank statement is a list from your bank showing all your account’s transactions. Bank reconciliation is when you check that list against your records to make sure everything matches up and to find any mistakes. This helps keep your money records accurate and secure.

How DocuClipper Can Help with Bank Statements & Bank Reconciliation?

DocuClipper simplifies the bank statement conversion and simplifies bank reconciliation process with its advanced features:

- Convert PDF Bank Statements: DocuClipper can convert any PDF bank statements into Excel, CSV, or QBO formats in seconds, making it easier to analyze and reconcile transactions.

- Categorize Bank Transactions: Automatically categorizes transactions using keywords. This helps in quickly identifying and matching transactions during reconciliation.

- Analyze Bank Transactions from Bank Statements: Provides insights on cash flow, spending, income vs. expenses, and more, aiding in a more comprehensive reconciliation process.

FAQs about Bank Reconciliation vs Bank Statement

Here are some frequently asked questions that people ask about bank reconciliation and bank statements:

What is the difference between a bank statement and a reconciliation?

A bank statement is a summary of transactions provided by the bank, while bank reconciliation is the process of ensuring your financial records match the bank’s statement.

What is the difference between a bank statement and a bank account?

A bank account is an arrangement with a bank where you can hold and manage your money, whereas a bank statement is a document showing the transactions in the account over a period.

What is the difference between a bank statement and a bank ledger?

A bank ledger is an internal record of all transactions affecting a bank account, maintained by the account holder or their accounting system. A bank statement is the bank’s version of this record.

What is the difference between a bank book and a bank statement?

A bank book, often referred to as a passbook, is a booklet given by the bank showing deposits and withdrawals. A bank statement is a more detailed record issued periodically that includes additional information like fees and interest.

What is a bank reconciliation statement?

A bank reconciliation statement is a document that matches the cash balance on a company’s balance sheet to the corresponding amount on its bank statement, reconciling any differences.

What two items do you need to reconcile your checking account?

You need your bank statement and your record of transactions (like a check register or accounting software).

What are the red flags on bank statements?

Red flags include unrecognized transactions, repeated payments to unfamiliar recipients, and unexpected fees or charges.

How to prepare a bank reconciliation statement?

To prepare a bank reconciliation statement, start by comparing your transaction records against the bank statement to ensure they align. Next, adjust your balance for any checks or deposits that haven’t cleared yet. Then, add or subtract any bank fees or interest that haven’t been recorded in your books. Finally, adjust your records so your ending balance matches the one on the bank statement, ensuring your financial records are accurate and up-to-date.

Related Articles:

- Purchase Order vs Invoice: What are the Differences

- Outsourced Bookkeeping: Benefits, Costs, and How To Outsource Bookkeeping

- OCR Data Extraction: How to Use It for Your Business

- How to Read a Bank Statement and Actually Understanding It

- Benefits of OCR for Family Law Industry

- Bank Statement vs Credit Card Statement: Definitions, Differences, & Roles of Them

Next step

Automate your bank statement reconciliation

Start free. Upload a statement and see extracted transactions reconciled against the statement's balances. Export to Excel or QuickBooks when ready.